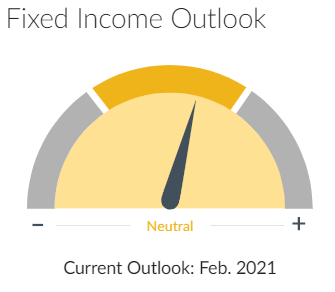

What we see

An improving outlook as the virus moderates, vaccine distribution improves and additional stimulus becomes more likely continues to bias rates higher and create tailwinds to credit sectors. The Federal Reserve remains fully committed to its accommodative stance and letting inflation run above the 2% target. Recent concern about the Fed tapering asset purchases is premature in our view. Heavy demand for dollar-based fixed income assets both domestically and abroad will likely keep any rate rise limited. We continue to favor credit risk over rate risk for both corporate and municipal bonds as well as structured credit. Sector differences will likely be significant as the economy we are recovering to will be different than the pre-pandemic economy and we remain highly selective in the current environment.

{kind=link}